December 15th is the deadline to choose a healthcare and/or dental benefit plan through the healthcare exchange.

One of the goals of the healthcare exchange, as a part of the Affordable Care Act, is to help you to compare plans and benefits to ensure you are choosing the best plan for yourself and your family.

However, if you still have questions or are feeling confused about how to compare dental provider networks, benefit levels, deductibles, minimum coverage, coinsurance, waiting periods, and all of the other jargon you see, you are not alone.

Our patients and followers on social media have been asking questions about how to compare and select policies. We are collecting those questions and providing responses here on this page for you to use as a guide to dental insurance through the healthcare exchange.

PLEASE NOTE: We cannot tell you which specific insurance plan to choose, nor are we endorsing any particular plans, benefits or carriers. Our goal is to help you understand how plans are built, to understand the words and terms used, and where to find potential hidden exceptions to ensure you get the care and coverage you need while minimizing potential out of pocket expenses.

Frequently Asked Questions: A Guide to Dental Insurance Through the Healthcare Exchange

Click on the (+) below to expand the question and read our response.

Don’t I already have dental coverage with SmartPlan Choice through Medicaid?

SmartPlan Choice is one of the new plans that provide coverage for adults and children who receive support through Medicaid. SmartPlan Choice is administered by DentaQuest. The SmartPlan Choice or DentaQuest websites do not contain specific information about the benefits contained in the plan for adults. To find out what benefits are offered for adults under this or any other HFS/Medicaid plan, we suggest contacting your dental care provider directly to review the benefits and coverage levels.

To find a dental provider who is enrolled with your plan, or find out what plan you are enrolled with, use this site to enter the member’s information to confirm the plan and research the benefits, or search by your location or provider name.

If you are interested in learning more about the coverage offered by your plan, or to learn about coverage for other plans we are enrolled with, we encourage you to contact your 1st Family Dental home office. We may not recommend any specific plan to you, but we are happy to provide you with information and answer your questions so that you can make the most informed choice possible.

According to a memo by the Department of Human Services, members may change their plans once during the initial 90 days of signing on, and then once per year after that. You can review the basic services offered by each of the available plans here.

What’s the difference between the dental benefits that are included in a medical plan, and stand-alone dental plans?

This question came from Jennifer, via email.

The answer to this question is a bit tricky, and depends on what’s contained in the plan, and how the benefits are administered.

In short, some medical plans also offer dental coverage.This is separate from a stand-alone dental insurance plan for individual or family.Here are some important questions to consider for medical plans that include a dental benefit:

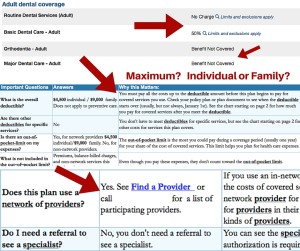

Will I need to meet my medical deductible before I can receive dental benefits? In many plans, dental coverage is subject to the individual or family deductible.That means you must pay out of pocket for any non-preventive services you receive, up to the deductible amount, before dental coverage would kick in.

Is there a maximum covered amount?Most plans include a maximum allowable amount for the plan year, such as $1,000.

Are there limits or exclusions to coverage?Is coverage only available for adults or children?Is treatment limited in how often it will be covered in a given period (such as once every 3 or 5 years)?Does the coverage exclude certain types of treatment?Some plans exclude major treatment such as root canals or crowns, for example.

Do I need to see a provider in-network?If the answer is yes, your services may be subject to the out of network deductible and/or lower coverage rates, which is typically higher than the in-network deductible.

Stand-alone dental plans require that you pay a separate monthly premium, which will increase your monthly healthcare costs.However, depending upon how much treatment you or our family members may need, especially major treatments like root canals and crowns, or orthodontics, your total out of pocket expenses may be lower with a separate dental plan.

In addition, many dental plans also cover some or even all preventive services such as routine checkups and cleanings, which can prevent the need for major treatments down the road, and reduce potential (and unexpected) out of pocket costs, saving you money in the long run.

Take a look at this summary of a medical plan with dental benefits included, and our markups:

Do I have to buy dental insurance for my 5 month old? He doesn’t even have teeth yet!

This question was submitted by Dave, from our Facebook page.

The short answer is, “no.” Parents are not required to purchase dental insurance for their children. However, pediatric dental care has been listed as one of the 10 essential health benefits (EHB) that all insurance carriers must include on policies that are available on the Healthcare Exchange.

Illinois is one of the states that expanded Medicaid eligibility. This means the income threshold for you or your children to be eligible for health and dental care through state programs such as All Kids has been raised. Purchasing a plan through the Healthcare Exchange is based on reported income, and some folks are eligible for subsidized coverage, or reduced premiums. It is important to note that while all plans on the exchange must meet a certain standard of included benefits when it comes to pediatric or adult dental care, not all coverage is the same. We will review some of the available plans in a separate post.

Our dental insurance is through my spouse’s job. Does this apply to me?

This question was submitted by Vicky, from our Facebook page.

If your dental insurance is covered by your employer or your spouse’s, you will need to follow the open enrollment period determined by the employer, and choose from the plans available. However, dental policies contain much of the same elements whether they are available on the healthcare exchange, or through an employer.

We’ve developed a 3-part guide on how to understand and select a dental insurance policy that anyone can use. Part 1 of the guide helps you to understand the different types of general plans available. Part 2 helps you to assess what kind of services and coverage you and your family may need, and what questions to ask the insurance carrier about the plan. Part 3 provides a guide to help you select a dental provider that not only accepts your insurance policy but will help you to get the best care and value from your plan, while minimizing out of pocket costs.

What is a waiting period and how does it affect coverage and benefits?

A: A waiting period is the amount of time (usually in months) that a person must wait before that service or treatment will be covered by the insurance policy. Typical waiting periods are 6 months and 12 months.

Example: Some dental policies include a 12 month waiting period for “major” procedures. That means you have to be enrolled in the plan for at least 12 months before the benefits in the plan will cover the procedure. Major procedures typically include crowns, dentures, implants and oral surgery, although they can vary by plan or provider.

How this applies to you: If you or someone on your policy is in need of major treatment before the waiting period is over, you will be expected to pay for the procedure out of pocket, even though the procedure is technically “covered” under the policy. This is why it is important to carefully review the exclusions for each plan. A plan may have a lower monthly premium, but may end up costing you more in the long run because of exclusions like waiting periods.

What questions do YOU have? We want to know! Ask your question in the comments section below and we’ll respond to each one. We’ll be sharing the most common and interesting questions about dental benefits and policies and our answers on Facebook and Twitter, so follow us to keep up!

Leave a Reply

Comment